J.S. Bach at Oracle Open World

Double Violin Concerto D-Minor BWV 1043, Xiaobin and Alina - Violin, Hans - Cello

It seems to be difficult to enter, balance and eliminate inter- and intra- company transactions when there are multiple balancing segments in a chart of accounts. It need not be so. We can make it easier - here are some thoughts and suggestions. What do you think?

This document is limited to a discussion of balancing inter and intra companies in software ledgers that support multiple balancing segments, such as Oracle's General Ledger Cloud Service.

Let's look at the terminology and make some definitions and distinctions.

Inter-Company & OwnershipInter-company is a phrase used by the FASB and IFRS to refer to updates of legal ownership between legal entities under common ownership or control. The words mean "between companies".

Intra-Company & Responsibility

Intra-company is a phrase used to discuss updates of management responsibility. Management individuals are classified by management organizations and are responsible and accountable for successfully creating transactions that increase the ownership of the legal entities. They "own" the transactions in the sense of being responsible for them, but not in the legal sense.

The words intra-company mean "within a company". An intra-company update implies that one team of employees in the company of an item owned has been made responsible for the item, rather than another team.

Inter and Intra togetherEvery update of ownership within a group carries a change in responsibility. The managers employed by the selling legal entity are no longer responsible for the item sold, and managers in the buying legal entity are assigned responsibility. This is true even when the managers in both organizations report to the same worldwide organization. The responsibility often changes on a transfer of ownership. A sale of inventory from a manufacturing company to a sales subsidiary will involve a shift of responsibility from "manufacturing" to "marketing", for example.

Balancing SegmentA chart of accounts (list of accounts in a General Ledger) is a way of tagging transactions so that they can be classified by owner, responsibility, function, nature and other attributes. Detailed transactions are aggregated by these tags. The different tag types are called segments, and each segment has a list of values, one value for each "tag" in that segment. Company codes are a fine example of tags.

A balancing segment is a segment where the debits and credits always equal each other within a given value (BSV). Software makes this happen by creating a due-to and due-from entry within each value when the user writes an entry that crosses values.

ExampleYou wrote an entry that credited company 100, cash for $1000, and debited company 200, cash for the same amount. Your software would add two lines to the journal, as shown in red, so that both companies had a complete set of debits and credits and therefore balanced:

As the company codes in the illustration are company (LE) Codes, this example is a basic inter-company entry, updating ownership. Were they not company codes but division codes, it would instead be a basic intra-company entry, updating responsibility.

Balancing segments are used where you need to track equity and a complete balance sheet and income statement.

Oracle EBS accommodates one balancing segment and many regular segments. EBS does not support multiple balancing segments.

The recommended deployment is to use the balancing segment for ownership by legal entities and regular segments for management responsibility. When people need the management responsibility to balance, they would either:

The Oracle General Ledger Cloud Service addressed this issue by providing multiple balancing segments. There is one primary balancing segment, and there are two secondary balancing segments. The primary balancing segment can be echoed in the Intercompany Segment. It is strongly recommended that you use the primary balancing segment to track legal ownership through the legal owner, the legal entity – that is, GAAP or IFRS recognition – and use the other segments for management purposes.

Folks are often intimidated by the idea of the Secondary Balancing Segments, particularly those who have been accustomed to the EBS approach. They are concerned that they will generate a great number of transactions. People are also concerned as to how to balance and eliminate responsibility accounting balances.

While relatively new to Oracle – the feature was introduced some ten years ago – it is not at all new in business. There is a long tradition of revising management responsibility at the same time as you update legal ownership and GAAP recognition.

So, let's distinguish between (a) the legal ownership transaction as the formal sale and purchase that it is, and (b) the responsibility update as a de-assignment and re-assignment to potentially, but not always, new managers.

This perspective worked before computers did, and it worked on mainframes, on mid-sized computers, on client server, on Unix & Linux boxes, and it will in the cloud.

The approach is (a) to acknowledge the stripping of responsibilities from the providing LE's staff before making the sale, then (b) to make the sale and buy without any responsibility transfer, and finally, (c) to have the second LE, once it has acquired ownership, assign the appropriate responsibility to its staff. This series of actions can be largely automated.

1.Before selling (de-recognizing an LE's ownership) a service or a product (the content) to a sister company, clear the management attribution associated with the content from it.

2. Execute the sale – transfer ownership to the recipient LE, recording an inter-company receivable.

3. At the acquiring company, record the buy, that is, the recognition of the new ownership of the content, and record a liability to the selling company.

4. Attribute management responsibility to the content as appropriate for the buying company.

a. This facilitates LE derivation during the close, improving close speed.

b .It dramatically reduces the number of cross-book transactions, also improving close speed.

c. Inter-company reconciliation is simplified, speeding the close by reducing the volume of work done during the close.

d. Inter-company elimination is simplified, also speeding the close

2. Intra-company activity is confined to individual Legal Entities. The selling company eliminates its own internal intra-company, and the buying company does likewise. There are no intra-company account balances on the legal entities' consolidated trial balances.

a. Intra-company reconciliation is executed by the LE controller, not the consolidation controller, that is, where the knowledge is, thus speeding the close.

b. It is not assumed that the selling company will understand the bookkeeping requirements of the buying company, reducing the risk of error.

c. The process can be largely automated, also reducing risk of error:

i. At the selling company, by availing of the standard balancing segment features (described earlier)

ii. At the buying company, by using Sub-Ledger Accounting (SLA) as configured and implemented in Accounts Payable, along with the GL & SLA balancing feature.

Before selling goods or services to a sister company, you can strip the accounting attributes tagged in the secondary balancing segments by intra-company updating them to common values that mean "no value". There are different ways to do this, depending on how you designed your chart of accounts, and the processes involved.

The possibility of automation in these cases can be a function of the process involved. The initial entry removing the local attributes at the source can be handled by the standard SLA (XLA) & GL balancing feature, and never includes any profit mark-up issues, as it is within the legal entity. The second entry from the Intra-account to the Inter-account must be addressed by the functionality one is using to generate the intercompany transaction.

At the receiver company, the entry from the intercompany account to the intra company account can be set-up using the intercompany functionality, and the management attribution can be handled by SLA's balancing feature.

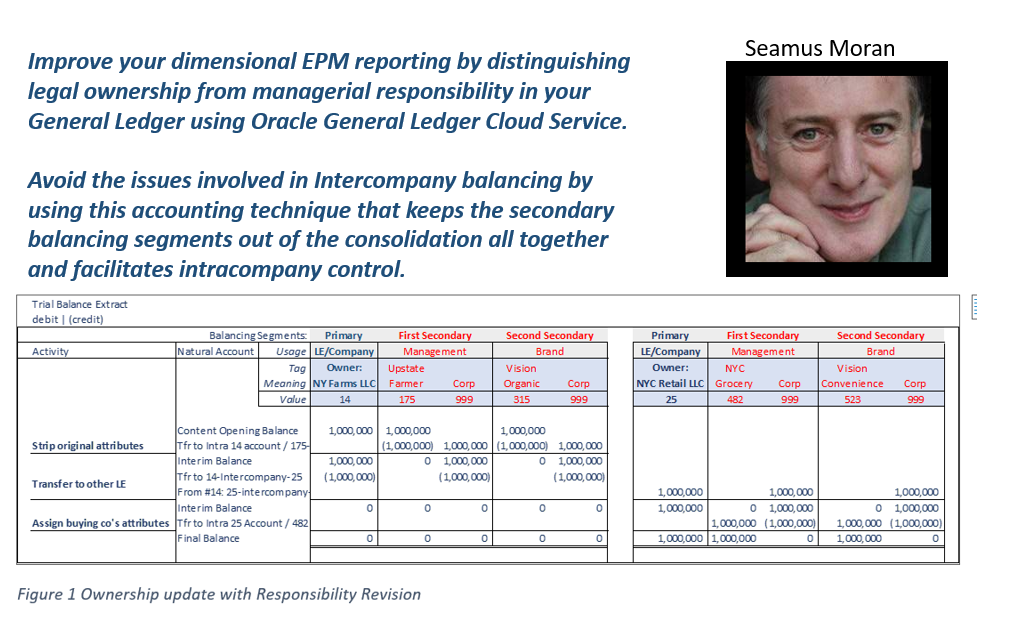

ExampleOur friends at Vision Farms operate a farm in Upstate New York, incorporated as New York Farms LLC, and managed by the Upstate Farmer team. A high-quality farm, its products are branded as Vision Organic.

New York Farms LLC transfer $1M worth of goods and services to another Vision company, Vision New York City Retail LLC, who operate stores in NYC and on Long Island, and is managed, of course, by the New York Grocery management team. These particular goods and services are destined for the Vision Convenience brand, sold through small stores at subway and LIR stations, where you can pick up fresh, healthy food on your way to and from the office in Manhattan. (City Retail view them as a Convenience Store sale, while New York Farms viewed then as an Organic sale.)

Vision tracks the ownership by LE in a primary balancing segment, their management teams in the first secondary balancing segment, and the brands in the second secondary balancing segment. The secondary balancing segments each have a 999 "corporate" value. Intra-company receivable & payables are all posted to a natural account called "Intra-charge". Inter-company business is charged to intercompany AR and AP accounts with the counter-party company code in an intercompany segment, for balancing & elimination.

This is an extended trial balance format. The columns represent the owners and managers. The horizontal lines include the T-accounts.

1. The illustration does not assign account numbers to natural accounts. Using a common chart of accounts, this text will use the following:

Inventory-4500; IntraCo Balances-9999; interco receivables-3500; interco payables-8500

2. In the beginning, $1,000,000 is coded to 14-175-315-4500 (inventory owned by Co. 14, attributed to 175 and 315.)

3. Intra Company balancing credits it there and debits it to 14-999-999-9999 (Intra Balances)

4. Inter Company accounting credits it to 14-999-999-9999, balancing 9999, and…

5. Debits it the intercompany receivable 14-999-999-3500-25, 14's intercompany receivable from 25.

6. On their trial balance, company 14 reports no inventory, nothing in 175 or 315, and nothing in 999, 999 or in 9999, and an intercompany receivable in 14-999-999-3500-25

7. On receipt of the charge, Company 25 credits the intercompany payable 25-999-999-8500-14

8. And debits 25-999-999-9999, in intra company "nobody" account

9. Intracompany credits the "nobody account" 25-999-999-9999, thereby balancing it, and debits whatever management team and natural account is appropriate: 25-482-523-xxxx (in this case 4500 for inventory.

10. On their trial balance, company 25 reports owning inventory, attributed to 482 and 523, and nothing in 999, 999 or in 9999, and an intercompany payable in 25-999-999-8500-14

11. In consolidation, there are no balances in 14-175 or 14-315. There is no balance in 14-4500. There are no balances in 9999, or in 999 or 999.

12. 14 does show a receivable from a sister company in 14-999-999-3500-25.

13. 25 does show a payable to a sister company in 25-999-999-8500-14

14. These obviously match and eliminate.

15. 25's inventory in 25-3500 is on the Group balance sheet as owned through company 25 and is attributed to the management teams 482 and 523.

16. The account 9999 has a zero balance on both trial balances and therefore on the group.

17. The management attributes 999 and 999 in both companies have zero currency values

There are other approaches to managing ownership and responsibility accounting together. This one has been tested by time and practice, and very much reflects the underlying principles.

Thank you

Seamus Moran

08/18/2022

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Comments 2

Hi Seamus,

Thank you for this post. I am thinking about your article and would like to ask two questions:

1) Would your approach change if the management organizations are crossing legal entities or even countries? Your example has distinctly different management units and brands on both sides of the transaction. I see "Upstate Farmer" and "Vision Organic" on the NY Farms LLC side versus "NYC Grocery" and "Vision Convenience" on the NYC Retail LLC side. How about both sides dealing with the same corporate wide management unit "Fresh Fruit and Vegetable" and brand "Certified Organic". What I am getting at is that the management units often will cross legal entities.

2) What would be the difference between two balancing segments and a parent-child structure? It seems that each secondary balancing entity is established within the legal entity structure. The total number of separate balance sheets would be the same, correct?

To be continued

Hans

Q1: No, the approach does not change. The assumption is that management acts both across legal entities, but by means of them. When the first LE cedes its ownership, it also cedes its responsibility; when the second takes ownership, it also takes responsibility. So the first LE goes from Co-Mgmt'x-Mgmt'm to Co-null-null at the sale; sells it to New-Co-null-null. The Bew Company goes from NewCo-null-null to NewC-Mgmt'x-Mgmt'm if the are the same, or to NewCo-other-other if not. The idea is that the first company's responsibility ends when it sell the item. So it intra balances should not be on its ownership balance sheet. The second company's responsibilities commence when it buys the item, and it debt for item is recognized in its inter-company account to the other company.

Q2: The multiple balance sheet feature provides a gauge of equity for management, the tree and hierarchy features do not. The number of ownership (true) balance sheets should correspond to the primary balancing segment's LE listing. You can create a management responsibility balance sheet for each value in each secondary balancing segment at every level from legal entity to total group.